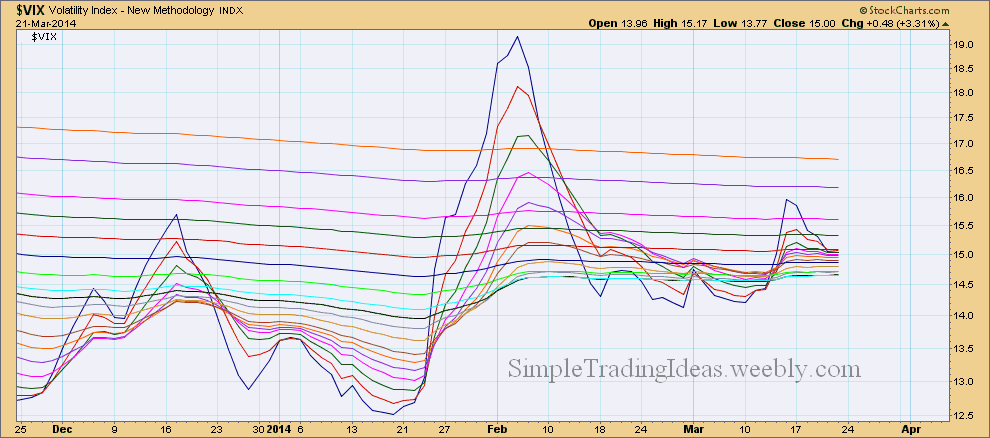

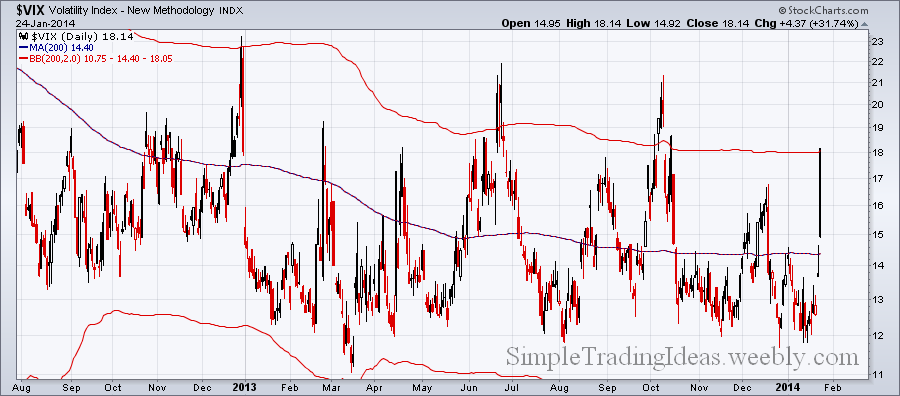

$VIX sharply moved lower during the past week showing that investors are having more confidence in this long-term uptrend and the recent "fear" of a deeper correction is now in the past. Even sudden geopolitical events only moderately affected the market as it was evident this past Friday and it was quickly absorbed showing how resilient is this equity market. $VIX spiked above the 200-day moving average but finished the day below that as fear dissipated during Friday.

RSS Feed

RSS Feed